Interest rates and real estate sales

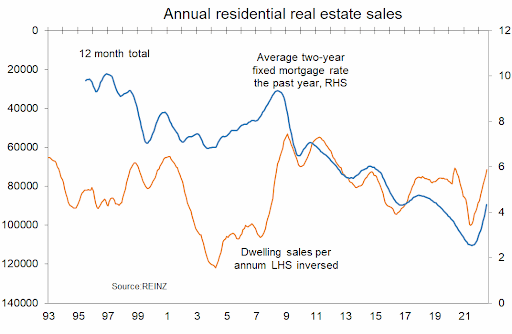

Here is an interesting graph. The orange line measures the total number of dwellings sold by licenced real estate agents for each 12 month period. It is measured on the left axis which is upside down. Why? Because the blue line shows the average two-year fixed mortgage rate which is measured on the right side.

When interest rates rise, we would expect sales numbers to fall away. That is represented by the blue line going up and the orange line following suit. The relationship is reasonably good.

The latest data show dwelling sales adding up to just over 70,000 in the year to July. But the data also show the average two year fixed mortgage rate sitting at 4.3%. This is a full percentage point below where the rate commonly sits currently.

So, what you need to do is in your head extend the blue line up another 1% and make a similar move to the sales total. You’ll see maybe we end up with annual sales at around 65,000 or so. Maybe less.

The more important point is that one shouldn’t really expect much of a recovery in dwelling sales until interest rates are heading back down again. That might not happen in a sustained manner until the latter part of 2023 all going well (best guess in this uncertain world). That means still challenging times for real estate agencies around the country over the coming 12 months with rationalisation in the sector to continue.

Sales growth is likely to be improving on a sustained basis over the second half of next year.

Interest rates below average - sort of

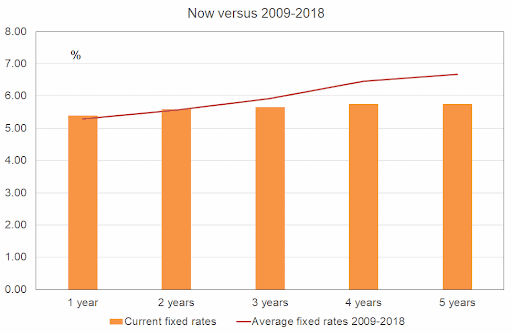

The average one year fixed mortgage rate currently sits at about 5.4%. The average two year rate is around 5.6% and the three year rate is near 5.7%. 15 months ago these rates were respectively 2.2%, 2.6%, and 3.0%.

We can reasonably say that there is an interest rates shock running through the economy, brought on by our central bank belatedly shifting to fighting inflation rather than preventing any pandemic – driven rise in the unemployment rate.

All attention is on the impact on the finances of those people who signed up for the low rates of 15 months ago and are now rolling into much higher borrowing costs.

There are four points worth noting which help explain why a housing and economic apocalypse is not underway despite interest rates rising more in 15 months than it took the same rates to rise less than 3% in four and a half years pre-GFC.

First, no-one borrowing at record low rates last year was left in any illusion with regards to the ability of such borrowing costs to remain at record lows. It was logical to expect that ending of the pandemic would see monetary policy tightened and it was obvious a year ago that we were not in recession and a day of adjustment was looming.

Second, only one-third of households have mortgages and the overwhelming majority of them have had their mortgages for many years during which principal debt levels have been reduced.

Third, banks required all borrowers to prove that they could service their mortgages with interest rates of around 6% - 6.5% before they would advance them the money to make a purchase. A substantial cash flow buffer exists for virtually all borrowers and with the labour market so extremely tight there will be very few people under employment and interest rate-driven servicing stress.

Fourth, the jump in borrowing costs from 15 months ago is large. But rates have only returned to about where they averaged in the decade leading into the extraordinary 0.75% easing of monetary policy in 2019.

The orange bars in the following graph show where fixed lending rates commonly sit at the moment. The red line shows averages from 2009 through to and including 2018.

Rates are below the average levels before the extraordinary circumstances of 2019’s deflation worries and the 2020-2021 pandemic environment.

Of course, other things have changed which tell us current rates are having a greater restrictive impact than back then.

- House prices are higher so debts are as a proportion of income.

- Credit availability has tightened up.