Auckland Property Market Commentary - May 2026

Outlook for Auckland region

New Zealand’s economic growth remained volatile during 2025. Prior to the Israeli and USA attacks on Iran, the expectation was for a gradual improvement in economic growth over 2026. The current Middle East conflict has increased the uncertainty of future economic activity, at least in the short term.

Increased energy costs and the risk to future supply is growing as the conflict continues. Israeli attacks on Iran’s energy infrastructure and their retaliatory strikes on other Middle Eastern countries' energy infrastructure are escalating the risks to global oil supply. The longer the conflict endures, the greater the medium to long term risks to our energy supply and costs.

Current low domestic interest rates and the lower relative value of the New Zealand dollar should continue to flow through to provide some support to economic activity in the short to medium term. However, the inflation rate increased by more than market expectations in the March 2026 quarter, increasing the likelihood of future growth in interest rates.

The outlook for the economy is complex, particularly with the uncertainty over the length of the current Middle East conflict. Higher energy costs will continue to flow through to higher inflation. The key issue is whether there is a short-term shock to prices or whether there is a more enduring impact which results in higher inflation in the medium term and the subsequent impact on monetary policy, net demand, and overall economic activity. In addition, the outcome of the general election in November this year is increasingly uncertain with the National Party’s support continuing to decline in recent polls.

Office market

Auckland’s office market is continuing to experience challenging market conditions. The general economic and business outlook has helped create an environment where prospective tenants lack urgency to commit to leasing deals.

Landlords have remained flexible and are prepared to offer tenants turnkey solutions and the opportunity to split floors into smaller tenancies. The level of incentives offered, particularly for secondary quality space, remains robust with some landlords prepared to offer deals over the cost and ownership of any fitout provided. The tenant flight to quality buildings has continued in 2025 with businesses optimising the area of space they require and taking the opportunity to upgrade while leasing a smaller tenancy footprint.

The trend to work remotely for one or more days during the week has continued and businesses continue to adjust the area of office space they need.

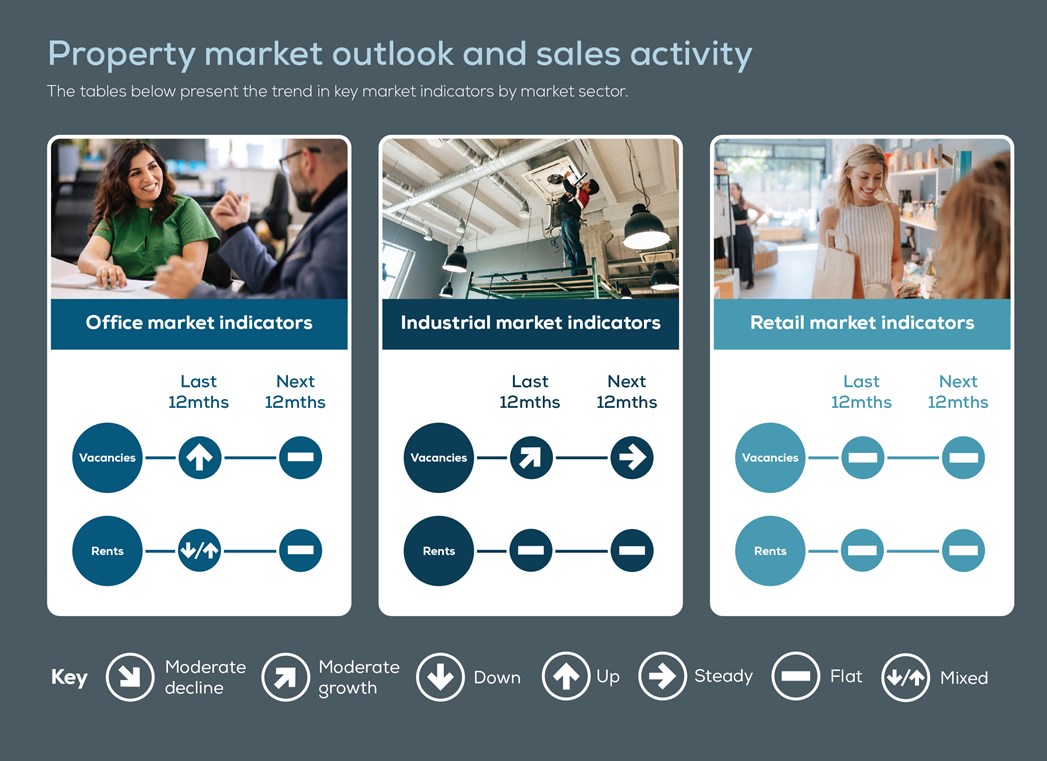

Vacancy rates within the CBD are now 15% up from 14% a year ago. The metropolitan office market has experienced a similar trend with the overall vacancy rate increasing from 10% 12 months ago to 11% in September 2025. Despite the increase in vacancy rates, market rents have remained flat over the last year.

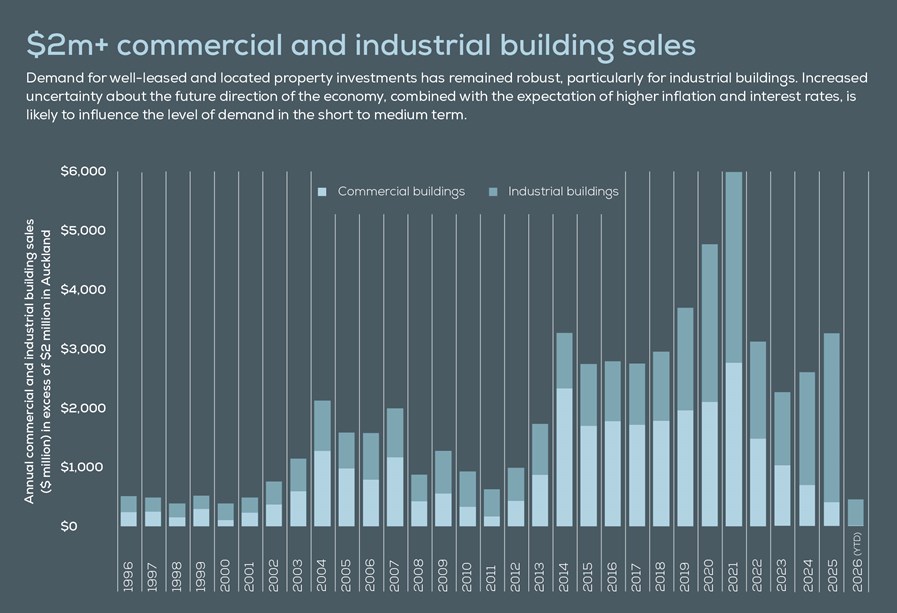

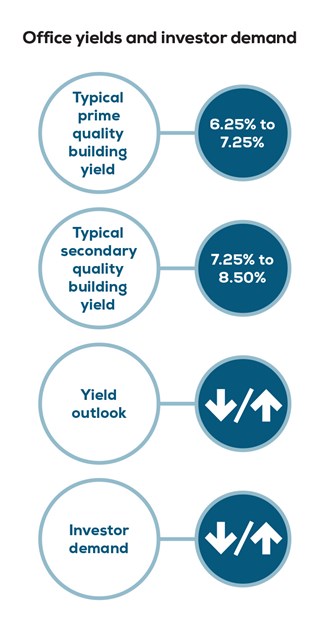

Investor demand and sales activity has continued to be mixed, with the uncertain economic outlook, high vacancy rates, mixed growth in tenant demand, and limited rental growth impacting on the volume of transactions. Falling interest rates may assist in boosting market demand for office buildings and place some downward pressure on yields.

Industrial market

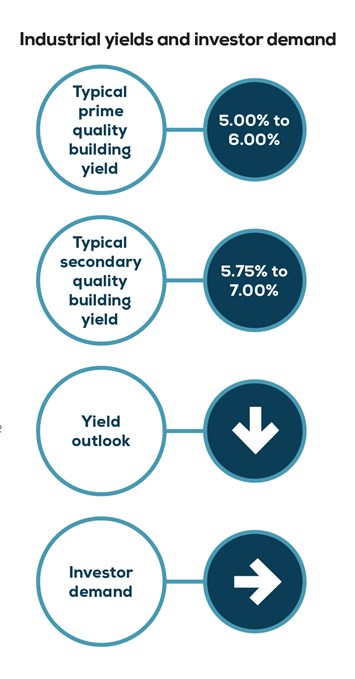

The industrial property market conditions improved during 2025. However, increased uncertainty over the future direction of the economy, higher inflation as a result of geopolitical instability overseas, and increased energy costs are likely to impact on business confidence and growth in 2026.

Tenant demand is mixed, and space with longer term vacancies are being offered with increased leasing incentives. Despite the softer market conditions in early 2026, the industrial market continues to outperform office and retail investments with higher levels of market activity and investment returns.

The number of building consents for industrial premises has remained robust with 136 consents issued for a total of 355,000m2 of space in the 12 months ended December 2025. This is up slightly from 131 consents with a total floor area of 311,500m2 in the previous 12 months. Consenting over the last two years has been lower than the previous six years (2018 to 2023) when the average annual number of buildings consented was over 200, with a total combined floor area of 430,000m2 of space.

A proportion of these buildings were speculative developments and although they have met tenant demand for new space, there is still some excess space available. In addition, development feasibilities remain tight with limited rental growth and rising construction costs. As a result, development activity has eased.

The market's overall vacancy rate experienced a small increase over the last six months increasing from 2.4% in June 2025 to 3.1% in December 2025. Although the amount of vacant space increased, it remains low at just over 3% of the total stock, reflecting the strong demand for space and a relatively tight demand/supply balance in the market.

Retail market

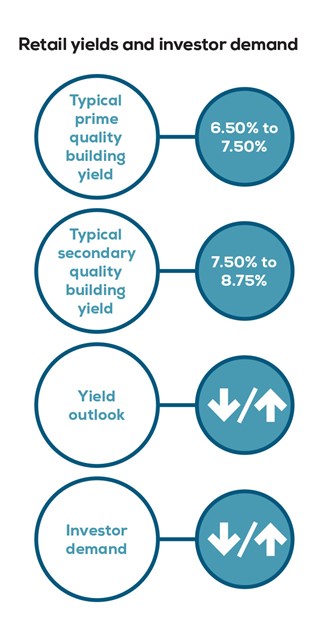

The outlook of New Zealand’s retail sector is mixed, with some areas performing better than others. The fall in mortgage interest rates over the last 12 months has provided households with some respite from the higher cost of living and has had a positive impact on consumer confidence and spending. However, the overall soft economic outlook and weak labour market conditions may weigh on the sector going forward.

Over the next 12 months, household spending was expected to gradually increase, with lower mortgage interest rates and moderate population growth boosting overall demand for goods. However, the outbreak of war in the Middle East will impact both economic and retail activity; the extent of which is difficult to predict. Interest rates are now expected to increase as higher energy and transport costs result in higher inflation. The higher cost of living is likely to place pressure on household budgets and constraint discretionary spending as households allocate a higher proportion of their budget to transport expenses.

The short-term retail property outlook is uncertain. The implications of overseas disruption to energy markets and global trade are impacting local economic activity and, as a consequence, tenant demand for retail space. At this stage, it is difficult to look through the short-term impact of recent events, however, in the medium term, tenant requirements for retail space will remain and the market will bounce back.

Our research

The market reports included in this publication have been prepared independently by Ian Mitchell from Livingston and Associates.

Every effort has been made to ensure the soundness and accuracy of the opinions, information, and forecasts expressed in this report. Information, opinions and forecasts contained in this report should be regarded solely as a general guide. While we consider statements in the report are correct, no liability is accepted for any incorrect statement, information or forecast. We disclaim any liability that may arise from any person acting on the material within.