August 2018 Auckland Property Market Commentary

Strong growth in Auckland’s economy has continued to drive the region’s commercial and industrial property markets. Robust market fundamentals combined with low interest rates have helped maintain investor demand for properties. However, the availability of credit is starting to impact on some potential purchasers limiting their ability to leverage deals.

- Auckland’s CBD and metropolitan office markets have continued their strong performance over the last year. Limited good quality vacant space available for lease in the CBD, combined with growing tenant demand has resulted in steady rental growth. These trends have resulted in moderate increases in development activity across the office market. The CBD office market is expected to continue its solid performance with expectations of further rental growth and strong tenant demand. The performance of the metropolitan market varies significantly by precinct. Uptake of space in the fringe city precinct has been strong and rents have continued to increase. The metropolitan office market has a number of developments due for completion over the next 12 months. These will provide back fill opportunities for some of the larger tenants currently looking for space. Investor demand continues to out strip the number of properties available for sale. Office building investments are continuing to provide strong annual returns with moderate income yields combined with ongoing value growth.

- Auckland’s industrial market has continued to provide investors with strong returns resulting from low vacancy rates, strong tenant demand, and increasing rents. Returns from this sector continue to outperform the office and retail property markets. The sector is continuing to display all the characteristics of a late cycle upswing. Auckland’s robust regional economy has driven a steady increase in occupier demand and this is expected to continue at least in the short term. Growth in demand has continued to place pressure on the amount of stock available to lease. Strong market fundamentals have resulted in increased construction activity. Demand for good quality investment properties is expected to remain strong as they are driven by a quest for yield.

- Retail property’s underlying market fundamentals have stabilised, and investment returns have been lower when compared to office and industrial buildings over the last 12 months. However, despite these trends retail property investments continue to be in demand and investment yields have not changed in recent times. The competitive environment for retailers remains intense and demand for well located retail space has not changed significantly. The rate of rental growth has slowed in the central city whilst modest growth is being experienced in regional centres. The outlook for the retailers is mixed and they are likely to experience ongoing challenges and intense competition. Demand for space in prime locations is expected to remain strong in the entertainment, cafes and hospitality sectors as they continue to grow.

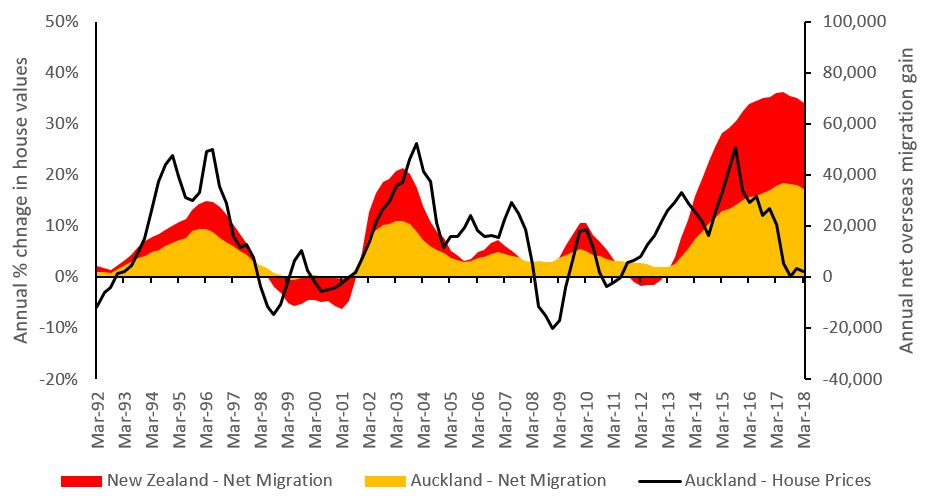

New Zealand’s economy has continued to expand over the last year. The current economic and business cycle is being supported by accommodative monetary policy, strong population growth driven by high net gains from overseas migration, and robust expansion in the tourism sector. Although Auckland region is expected to continue to grow faster than the national average, a general malaise in the business sector is impacting on overall confidence as people adjust to the new policy direction under the Labour led coalition. As a result, property owners appear to be more likely to hold their buildings rather than sell and seek new investment opportunities. These trends are not dissimilar to what happened when the Clarke led Labour Government was elected in the early 2000s.

Figure 1 presents the trend in net annual overseas migration combined with Auckland house values growth.

Figure 1: Net Overseas Migration and House Value Growth

Strong population growth, increased construction activity and low interest rates are likely to continue to underpin expansion in Auckland’s economy in the short term. However, a range of other factors have impacted on house value appreciation over the last 12 months resulting in little to no value growth. Housing affordability is poor and the Government’s move to ban foreign residents (estimated at 7% of total sales in Auckland) buying existing property is likely to impact on future growth.

Table 1 presents the trend in key market indicators by market sector.

Table 1: Property Market Indicators

| Office market | Industrial | Retail | ||||

|---|---|---|---|---|---|---|

| Last 12 months | Next 12 months | Last 12 months | Next 12 months | Last 12 months | Next 12 months | |

| Vacancies |

Flat | Up | Steady at low levels |

Steady | Steady at low levels |

Flat |

| Rents | Prime up Secondary up |

Up | Up | Up | Steady | Steady |

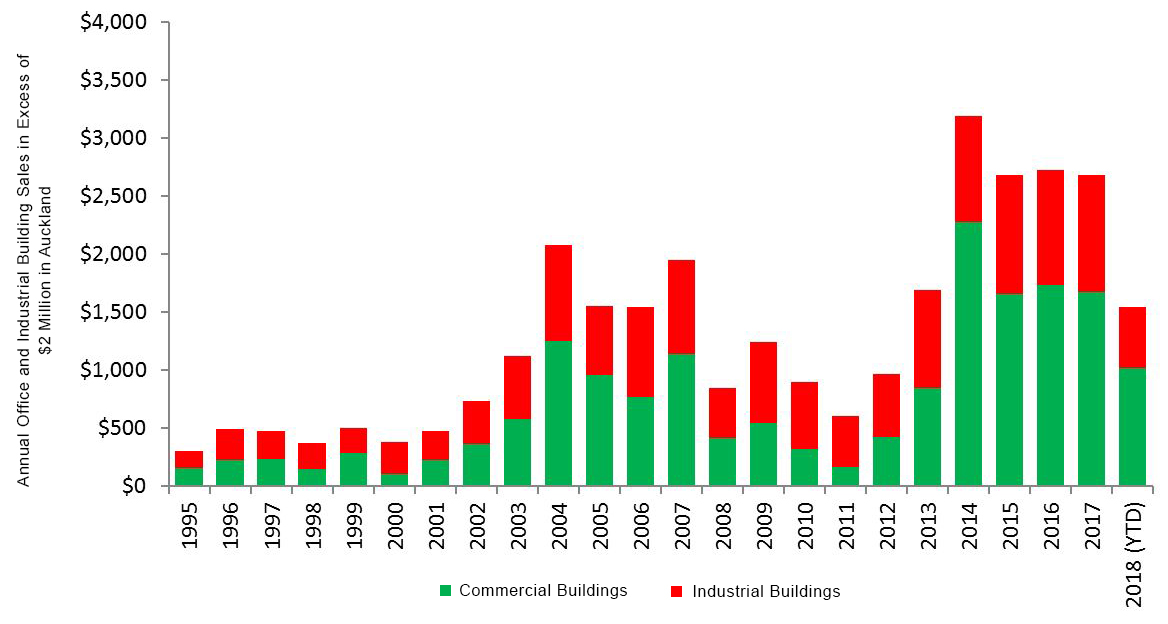

Figure 2 presents the growth in the value of commercial and industrial building sales in the Auckland region with sale prices more than $2 million.

Figure 2: Commercial and Industrial Building Sales (properties selling for more than $2m in Auckland)

Table 2: Yields and Investor Demand by Sector

|

Yields

|

|||||

|---|---|---|---|---|---|

| Sector | Typical prime quality building |

Typical secondary quality building |

Outlook | Investor demand | |

| Retail | 4.00% to 6.50% |

4.00% to 6.50% |

Steady | Strong | |

| Office | 5.50% to 6.50% | 6.25% to 7.00% |

Steady | Strong | |

| Industrial | 5.00% to 6.25% |

5.75% to 6.75% | Steady | Strong | |

Every effort has been made to ensure the soundness and accuracy of the opinions, information, and forecasts expressed in this report. Information, opinions and forecasts contained in this report should be regarded solely as a general guide. While we consider statements in the report to be correct, no liability is accepted for any incorrect statement, information or forecast. We disclaim any liability that may arise from any person acting on the material within.