October 2017 Auckland Property Market Commentary

Auckland’s commercial and industrial property markets have experienced another strong 12 months. The underlying market fundamentals remain robust with low vacancy rates, strong tenant demand, and low yields. However, the availability of credit is starting to have an impact on some potential operators particularly those looking to buy development sites.

- Strong regional economic growth combined with increases in the number of people employed in the key office occupying sectors has resulted in further expansion in the demand for office space both in the CBD and metropolitan office markets. Tenant relocation has impacted on the central city’s vacancy rate with a small increase in overall vacancy rates. For example, Vodafone has relocated its head office from the central city out to Smales Farm Office Park on the North Shore. However overall vacancy rates remain low and as a consequence rents have continued to increase over the last 12 months. Auckland’s metropolitan office market has continued to strengthen and vacancy rates are now close to 7%. Significant growth in demand from the social services sector has resulted in uptake of secondary quality office space in suburban sites as health service providers locate closer to their client base. For example, health service providers have been actively leasing space to provide mental health services in the suburbs.

- The industrial property market continues to experience strong market fundamentals with increasing demand, low vacancy rates, increased rents, limited land supply and strong investor demand. These conditions are typical of a late cyclical upswing. Demand is continuing to increase driven by robust regional economic growth. Land values for development sites remain high and, combined with rising construction costs, makes development feasibilities tight. Although rents have increased and yields have declined, there are building pressures for further rental growth. At the same time banks are becoming more risk averse. Anecdotal evidence suggests banks are rationing credit to developers which is impacting on their ability to respond to demand. Tight industrial land markets in the traditional greenfield precincts has resulted in increased interest in locations such as Drury to the south and Silverdale on the northern edge of the city. Improvements in the city’s transport infrastructure is likely to further redistribute industrial demand. Competition from residential developers is continuing to have an impact on light industrial redevelopment sites within the isthmus in locations that have been rezoned mixed use under the unitary plan.

- The retail sector is continuing to evolve with retailers further developing their online sales capacity. Expectations are for further growth in demand for space from the entertainment, café and hospitality sectors whilst retailers more exposed to online sales competition may struggle. Ongoing population growth should continue to drive overall sales growth, however this is likely to be unevenly distributed across different store types. Investor demand for well-located retail building investment opportunities remains strong and yields remain at historical lows.

New Zealand’s economy grew in line with market expectations in the June 2017 quarter, increasing by 0.8%. The quarter’s growth benefited from a one-off boost in tourist spending (partly from spending by Lions rugby tour supporters and the World Masters Games) and a rebound from temporary disruptions in some sectors. The current cycle continues to be supported by accommodative monetary policy, strong population growth driven by high net gains from overseas migration, and robust expansion in the tourism sector. Uncertainty of the result of the outcome of September’s general election on the stability of any coalition formed may impact on the economy’s ability to expand. Auckland region’s economy is expected to continue to grow at above average rates. Table 1 presents the trend in key market indicators by market sector.

Table 1: Property Market Indicators

| Office market | Industrial | Retail | ||||

|---|---|---|---|---|---|---|

| Last 12 months | Next 12 months | Last 12 months | Next 12 months | Last 12 months | Next 12 months | |

| Vacancies |

Flat | Up | Steady at low levels |

Steady | Steady at low levels |

Flat |

| Rents | Prime up Secondary up |

Up | Up | Up | Steady | Steady |

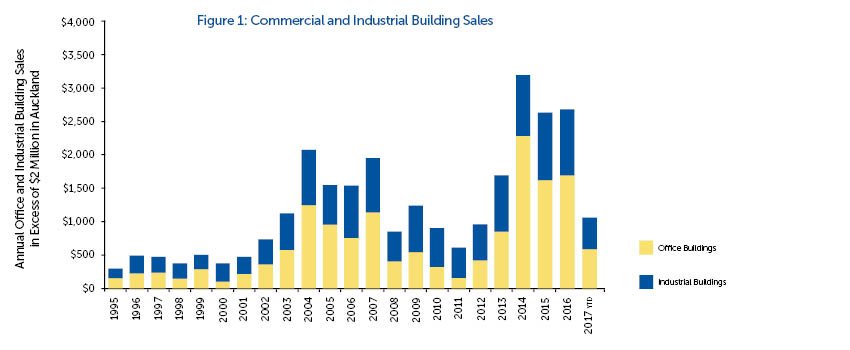

Figure 1 presents the growth in the value of commercial and industry building sales in Auckland region with sale prices more than $2 million.

The volume of sales remains robust however a lack of good quality stock available for sale is limiting the volume of sales activity. Current low interest rates are continuing to support investor demand. Table 2 summarises current yields by sector, their outlook over the next six months and the level of investor demand.

Investment market conditions are expected to remain robust in the short term. A number of factors are supporting current market conditions and these include current low interest rates, reasonable access to credit, strong growth in tenant demand for space resulting in low vacancy rates and strong competition between potential purchasers for buildings being offered for sale.

Table 2: Yields and Investor Demand by Sector

|

Yields

|

|||||

|---|---|---|---|---|---|

| Sector | Typical prime quality building |

Typical secondary quality building |

Outlook | Investor demand | |

| Retail | 4.00% to 7.00% |

4.00% to 7.00% |

Steady | Strong | |

| Office | 5.50% to 6.75% | 6.50% to 7.50% |

Steady | Strong | |

| Industrial | 5.00% to 6.25% |

5.75% to 7.00% | Steady | Strong | |

Every effort has been made to ensure the soundness and accuracy of the opinions, information, and forecasts expressed in this report. Information, opinions and forecasts contained in this report should be regarded solely as a general guide. While we consider statements in the report to be correct, no liability is accepted for any incorrect statement, information or forecast. We disclaim any liability that may arise from any person acting on the material within.